Buying a Home in British Columbia

Buying a Home in British Columbia

Buying a home is the largest investment most of us ever become involved in. Yet people sometimes take less time over it than they do when buying a new car. That’s because it’s unfamiliar territory to many of us. We don’t know what questions to ask. We may take things for granted, rely on others when we shouldn’t, and sometimes we later wish we had known more about the process involved.

It is important for you to understand the the process that is normally involved in the purchase of a home, to recognize the significance of the documents you will encounter, and to understand the role of other people who may be involved in the transaction. Buying a home is a major event. This information will help you better understand the entire process.

The Decision to Purchase

Purchasing a home can be both exciting and frightening!! It is probably one of the biggest financial investments you’ll ever make. You’ll not only have to live with your decision, but also live in it, so you don’t want to make any costly mistakes. Before you start looking for your “dream” home, organize yourself by considering a few basic questions:

What are my housing needs?

What are the choices?

What can I afford to spend?

Time spent answering these questions in advance may save you from frustration and disappointment during your search.

Types of Housing Structures

To meet the many kinds of needs that people have, a number of different housing styles and types of ownership have developed over the years. Your individual requirements and your income level will govern the housing type which is most suitable for you at the present time.

Single Family, Detached Home – A detached home is one which has no common walls with any other residential structure, resting on its own land with front, rear, and side yards. It may be any size from a small, one-storey bungalow to a huge mansion.

Semi-Detached Home – A semi-detached home is two single family dwellings joined together by a common middle wall. It is sometimes called a “side-by-side” duplex.

Duplex – A duplex is two separate dwellings which are attached either side-by-side (a semi-detached home) or one unit above the other. It is important to note that this type of structure may be a strata titled property and therefore subject to the Strata Property Act.

Townhouse – In British Columbia, the term “townhouse” is usually used to describe one of a group of dwellings (most often two-storey) joined together by common walls, each with its own entrance from the outside.

Apartment – An apartment is one of several dwellings (most often single storey dwellings built one above the other) joined together by common walls, each having its entrance from a common hall. The overall building containing the apartments may be from three to 33 or more storeys.

Mobile or Manufactured Home – A manufactured home is a factory-built residential structure designed to be moved from one place to another, although wheels are not necessary. It is often placed on a rented space (called a “pad”) in a manufactured home park.

Types of Housing Ownership

While there are a variety of housing ownership interests, the most common include the following:

Freehold – A freehold interest (also known as a fee simple) is the more precise term for what we ordinarily refer to as “ownership” of a home. The owner of the freehold interest has full use and control of the land and the buildings on it, subject to any rights of the Crown, local land-use bylaws, and any other restrictions in place at the time of purchase.

Freehold – A freehold interest (also known as a fee simple) is the more precise term for what we ordinarily refer to as “ownership” of a home. The owner of the freehold interest has full use and control of the land and the buildings on it, subject to any rights of the Crown, local land-use bylaws, and any other restrictions in place at the time of purchase.

Strata Title – The strata title form of ownership is designed to provide exclusive use and ownership of a specific housing unit (the strata lot) which is contained in a larger property (the strata project), plus shared use and ownership of the common areas such as halls, grounds, garages, elevators, etc. This type of ownership is used for duplexes, apartment blocks, townhouse complexes, warehouses, and many other types of buildings. In additiion, some single family home developments may be part of a bare-land strata development. Because ownership of the common space is shared, the owners also share financial responsibility for its maintenance.

Leasehold – In some cases, you might purchase the right to use a residential property for a long, but limited, period of time. The owner of this right of use has a type of ownership called a leasehold interest. This type of ownership is used most often for townhouses or apartments built on city-owned land. It is also used occasionally for single detached homes on farm land, on First Nation reserves, and for apartments where the owner of the freehold interest of an entire apartment block sells leasehold interests in individual apartment units to other “owners.” Leasehold interests are frequently set for periods of 99 years, but regardless of the length of the original term, you will only be able to purchase the remaining portion. Of course, the shorter the remaining portion, the less you, or the person who eventually purchases from you, will be willing to pay for the leasehold interest.

Cooperative – In the cooperative form of ownership, each owner owns a share in a company or cooperative association which, in turn, owns a property containing a number of housing units. Each shareholder is assigned one particular unit in which to reside.

What Can You Afford?

Before you start looking for a new home, it is important that you become aware of how much you can afford to pay. This knowledge will allow you to spend your valuable time looking productively at homes which are within your predetermined price range. You can calculate a relatively accurate figure for yourself if you assemble the following information:

The cash you have saved to be used for this home purchase is called the down-payment.

Plus: The amount of borrowed money you are able to arrange.

Less: Closing costs and other “last minute” costs associate with the real estate purchase.

Equals: Maximum Price

The Down-payment

Lending institutions will usually require you to make a down-payment of at least 5% to 10% of the purchase price of the home. Lending institution policies may vary from time to time. However, as a general rule, you should make your cash down-payment as large as possible. Your deposit for the real estate transaction may form part of your down-payment.

The Borrowed Money

Almost everyone who purchases a home borrows some of the money needed to pay for it. The easiest way to determine how much money you will be able to borrow as a mortgage loan is to consult with one or more lending institutions. These lenders will apply standard tests, based on your family’s current income and debts, in order to decide the amount of money they will lend to you. They will ask for information about your finances and make a thorough credit check, in order to be sure you are able to repay a loan.

What is a Mortgage?

Obtaining a loan to finance the purchase of your new home will probably require you to sign a document called a mortgage. This document will set out the terms and conditions for the loan and its repayment. If you fail to meet your debt obligations, the lender may have the right to claim your home to pay off what you still owe.

Obtaining a loan to finance the purchase of your new home will probably require you to sign a document called a mortgage. This document will set out the terms and conditions for the loan and its repayment. If you fail to meet your debt obligations, the lender may have the right to claim your home to pay off what you still owe.

Read our Mortgage FAQ HERE

What Types of Mortgage Loans Are There?

There are two basic types of mortgage loans:

- A conventional mortgage loan allows you to borrow up to 75% of the purchase price or the appraised value of the home, whichever is less.

- A high-ratio mortgage loan allows you to borrow more than 75% of the purchase price or the appraised value of the home, whichever is less. But the borrower must pay a mortgage default insurance premium to protect the lender if payments are not made. Check with your lender to find out the amount of the insurance premium.

Read our Mortgage Terminology helper HERE

What is an Amortization Period?

Typically, the size of a mortgage loan payment is calculated as if the loan payments were going to be paid over 20 or 25 years. This is called the amortization period. Each payment will repay the interest due up to the payment date along with some of the principal owed. The longer the amortization period you choose, the lower the regular payment will be. Keep in mind that the faster you repay any money borrowed by choosing a shorter amortization period, the more you reduce the total cost of borrowing.

What is a Term?

Most mortgage loan contracts only permit the regular payments to continue for a specified term which is shorter than the amortization period. The term can be as short as six months or it can be five years or more.

At the end of the term, you are required to repay the full unpaid balance. If you don’t have the cash required to pay the balance, it may be necessary to refinance the loan.

Deciding on the length of term you want will depend partly on whether you think interest rates will go up or down. Keep in mind that the longer the term you choose, the longer your monthly payment remains stable.

CAUTION: The lender is not obligated to renew your mortgage loan at the end of the term.

How Much Can You Afford to Pay in Mortgage Payments?

Based on Your Income:

A general guideline is to allow no more than 30% of your gross monthly income (before deductions) to make your monthly housing payments. This test of your ability to repay a mortgage loan is generally referred to as the Gross Debt Service Ratio.

Try our FREE mortgage calculator HERE

Complete the following calculation to determine the approximate amount you may be able to afford for the mortgage payment, the property taxes and, where applicable, 50% of the strata maintenance fees. Some lenders will require that this total maximum monthly payment also covers heating costs.

- Your gross monthly income $___

- Co-signor’s gross monthly income (if applicable) $_____

- Other income (monthly) $______

- Total monthly income $______

- Multiply the Total line above by 30% to calculate your: Total monthly maximum housing payment $______

Based on your Other Financial Obligations:

If you have other monthly financial obligations, such as car or credit card payments, the lending institution will also apply the Total Debt Service Ratio test to determine the maximum mortgage loan for which you can qualify.

A general guideline should be that the total of your monthly housing payment added to your other monthly debt payments should not exceed 40% of your monthly gross income.

The Gross Debt Service Ratio and the Total Debt Service Ratio tests protect both you and the lender by ensuring that you do not take on more debt that you can reasonably afford to repay.

Many lending institutions will prequalify you for a specific size and type of mortgage loan before you begin searching for your new home. Taking the time to apply for a pre-approved mortgage will give you the security of knowing how much you can afford to spend.

Before concluding the loan agreement, most lending institutions will require an appraisal of your selected home. The appraised value is a professional opinion of the value of the home and may differ from the purchase price you are willing to pay. The appraised value may affect the approved value of the loan.

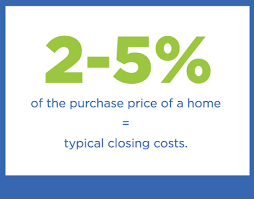

The Closing Costs

The Closing Costs

It’s easy to count your available cash, but remember that all of these cash savings cannot be used as your down-payment. There are last-minute costs, such as taxes, legal fees, appraisal fees, moving expenses, and home insurance to pay before you are finally in your new home. The time to budget for those “end” expenses is now. You must be prepared to pay most, and perhaps all, of the following closing costs.

Property Transfer Tax – The British Columbia Provincial Government imposes a property transfer tax, which must be paid before any home can be legally transferred to a new owner. Some buyers may be exempt from this tax. For further information, please view the Property Transfer Tax office website at www.sbr.gov.bc.ca/business/Property_Taxes/Property_Transfer_Tax/ptt.htm.

Goods & Services Tax – If you purchase a newly constructed home, you may be subject to GST on the purchase price. There may be some rebates available depending on the value of the home. For further information, contact the Canada Revenue Agency at www.cra-arc.gc.ca.

Property Tax – If the current owners have already paid the full year’s property taxes to the municipality, you will have to reimburse them for your share of the year’s taxes.

Appraisal Fee – When the lending institution requires an appraisal of the home before approving your loan, it may be your responsibility to pay the appraiser’s fee.

Survey Fee – The lending institution may also require that a survey certificate be presented to them. The purpose of the survey is to formally establish the boundaries of the property and to ensure that all buildings are within those boundaries.

Note: Lending institutions may ask for either a building location survey, which establishes where a building is located on a property, or a monumental survey, which establishes the actual boundaries of a property. If the current owner cannot provide a recent survey certificate, it will be your responsibility to pay the surveyor’s fee.

Mortgage Application Fee – Lending institutions may charge a mortgage application fee. This application fee may vary between lending institutions.

Don’t forget about last minute costs

Mortgage Default Insurance – This type of insurance is required on most mortgage loans in excess of 75% of the appraised home value. Its purpose is to ensure that the lender will not lose any money if you cannot make your mortgage payments and the value of your home is not sufficient to repay your mortgage debt. The insurance premium is paid to the lender and, in most cases, is added to the loan amount and paid for over the term of the

loan.

Life & Disability Mortgage Insurance – At your option, you may purchase insurance which will ensure that your outstanding mortgage balance is paid if you die or become disabled.

Fire & Liability Insurance – The mortgage lender will insist that you purchase an insurance policy which guarantees that, in the event of fire, the lender will receive the balance owing on the mortgage loan before you receive any insurance proceeds.

Legal Fees – The transfer of home ownership from the seller to the buyer must be recorded in the Land Title and Survey Authority Office in order to protect the new owner’s interests.

You will probably want to engage a lawyer or notary public to act on your behalf during the completion of your purchase. The lawyer or notary public will charge a fee for this service, plus disbursements, including the Land Title Registration fee. If you are financing your purchase with a new mortgage loan, there will be a further fee and disbursements to prepare and register the mortgage documents.

Other last-minute costs you shouldn’t forget to set some money aside for:

- home inspection fees

- moving expenses

- deposits required by utility companies

- household goods:

- kitchen appliances,

- garden equipment,

- garbage cans, tools, window coverings, etc.

- redecorating or renovations

Where Should You Purchase?

Where Should You Purchase?

Before you begin looking for your new home, it is important that you consider the needs of all the people it must shelter and what effect their daily activities will have on your desire for a certain size or location, both now and in the future. Thinking about some of the following factors will help you determine where and what you should purchase.

Community

- Rural? Small town? Suburban? City?

- What facilities are available: shopping centres? places of worship? recreational facilities? hospitals? schools?

- Are property taxes comparable to those in other communities?

- Are there any future developments planned which you may not like?

- Are the sewage and water systems adequate?

- What is the availability and cost of utilities: electricity? gas? water?

- What public services are provided: police? fire protection? ambulance? garbage collection? mail delivery? snow removal?

Transportation

- Is there nearby public transportation available?

- Do you mind a long commute to work or to visit friends?

- Can you afford to drive to and park at your workplace?

- Will another car be needed for your partner to drive to work, to shop, or take children to school or other activities?

- Are major roads easily accessible?

Neighbourhood

- Is public and private property maintained to your satisfaction?

- What is the composition of families living nearby: quiet, mature people? teenagers? potential playmates for children?

- Are their incomes and lifestyles compatible with yours?

- Have home values risen, fallen, or remained stable in the recent past?

- Are there any known projects on the horizon which could substantially change the quality of the lifestyle or the home prices in the area? Do you feel comfortable with the current zoning regulations? Will they protect home values yet still allow you to use a dwelling in the way you envision: outdoor basketball hoops and barbecues? storing your boat? a home-based business? keeping chickens/rabbits/horses? cutting trees? high fences? a basement suite? etc. When you walk up and down the streets of the neighbourhood, can you picture yourself living there for several years into the future? Do you understand the effect of the registered bylaws of a strata corporation? For example, do the bylaws restrict your right to rent the property or prohibit pets? Could the bylaws affect your quality of lifestyle and/or impact or protect the property’s value in the future?

Dwelling

- Are you interested in brand new only? an historic, character home? an already renovated resale? a solid, older home that just needs redecorating? or can you purchase a “fixerupper” and do major renovations yourself?

- What combination of space do you require? Think not only about bedrooms, bathrooms and garages, but also about areas for hobby activities and children’s play; and storage for clothes, skis, bicycles, wind surfers, tools, garden equipment, etc.

- Is a large, well-equipped kitchen important to you? How about a fireplace? A large entrance hall? A sun deck? A pool?

- Would you prefer a small lawn and low-maintenance garden, or do you enjoy cutting grass and making things grow?

- Do you need a dwelling with room to eventually accommodate more children? Elderly parents? Inlaws? Do you require wheelchair accessibility either for you or your visitors?

- Are there any restrictions which could prohibit pets or rentals?

Schools

- What schooling is available: primary? high school? adult evening programs? college?

- How close are the schools and how do the students get there?

- Are the schools crowded?

- Is the sports program satisfactory?

- Do the students have a high achievement record?

- If your family has special educational needs, are these available?

Real Estate Licensees: Licensing Requirement

It is important to understand that in British Columbia, the person you hire to assist you to purchase your home must be licensed under the provincial Real Estate Services Act.

It is important to understand that in British Columbia, the person you hire to assist you to purchase your home must be licensed under the provincial Real Estate Services Act.

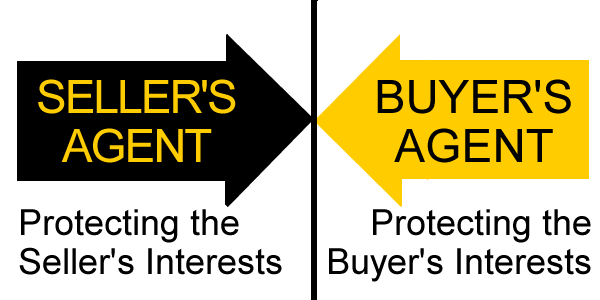

Responsibilities of Seller’s and Buyer’s Licensees

In every real estate transaction there is a seller and a buyer. A real estate licensee may be employed as an agent for the seller, as an agent for the buyer, or both. Early in the first meeting with a real estate licensee, the licensee should provide you with full disclosure about the nature of his or her relationship with you, as a buyer, and any relationship he or she may have with the seller. The licensee is required by law to provide this information and explain its implications to you.

Your Relationship with a Real Estate Licensee

When providing real estate services, the nature of the relationship that is created between the buyer or seller and the real estate brokerage, including its related licensees, is important. The relationship may be either a sole agency, limited dual agency, or no agency relationship. Be aware that these rules are changing in 2018 and the limited dual agency will change. Check back with us to get updates on these important new changes that affect you.

Sole agency

Where a licensee acts only for the buyer or the seller, a sole agency relationship is generally created. The buyer or seller who engages a licensee to act as a sole agent is known as the “client”. There are different types of sole agency relationships. The historical model of real estate agency, referred to in this material as ‘brokerage agency’, is one where the brokerage is the agent of the client, and all licensees engaged by that brokerage automatically assume the same agency obligations as the brokerage in relation to that client. When the brokerage only represents one client in a particular transaction this is referred to as ‘sole’ agency. Another type of sole agency, ‘designated agency’, occurs when the brokerage and the client agree that the brokerage will designate one or more licensees engaged by that brokerage to provide real estate services as sole agent to or on behalf of the client. In designated agency, the brokerage has contractual duties to the client but it is the designated agents who act as sole agent on behalf of the client.

As an agent, a licensee has certain duties to their clients. In addition to the general obligation that all licensees have to act honestly and with reasonable care and skill in performing all assigned duties, an agent has:

- a duty of undivided loyalty to the client;

- a duty to keep the confidences of the client;

- a duty to obey all lawful instructions of the client; and

- a duty to account for all money and property of the principal placed in the brokerage’s hands while acting for the client.

In designated agency, the brokerage and the client agree that these duties – other than the duty shared with the designated agents to keep the confidences of the client, and the holding of money on behalf of the client – are the responsibility of the designated agents.

Limited Dual Agency

When a brokerage acts for both the buyer and the seller, with their agreement, the nature of the relationship created by contract is one of limited dual agency. In brokerage agency, limited dual agency can occur when the same licensee engaged by the brokerage represents the buyer and seller, or where different licensees engaged by the same brokerage represent the buyer and the seller. Before a brokerage may represent both the buyer and the seller, the buyer and seller must consent to such a relationship. Before providing their consent, the buyer and seller should be fully informed regarding the limits that will be placed on the agent’s (brokerage’s) duties and obligations to the buyer and seller.

Designated agency allows two clients who have engaged the same brokerage to have independent representation by their respective designated agents, eliminating the occurrence of ‘in-house’ limited dual agency where the interests of those clients are in conflict, e.g. they wish to negotiate in relation to the same property.

Where a limited dual agency relationship has been agreed to, it is not possible for the agent (brokerage or its designated agent) to fulfill all of its duties to both parties. As a result, the duties are limited by contract and the sole agent, whether the brokerage or its designated agents as the case may be, become limited dual agents, with their duties being limited as follows:

- the brokerage and/or its designated agent must deal with the buyer and seller impartially;

- the duty of full disclosure is limited so that the brokerage or its designated agent are not required to disclose what the buyer is willing to pay for the property, what the seller is willing to sell the property for, or the motivation of either party; and

- the brokerage or its designated agent must not disclose personal information about the parties, unless authorized to do so in writing.

No Agency

A brokerage or its designated agent may also agree with a buyer or seller that they will not act as an agent on their behalf in a transaction. In other words, there will be no agency representation. In such a case, the buyer or the seller will be the “customer”, not the client of the brokerage or its designated agent. This may occur when a licensee already has an agency relationship with a seller, for example, and a buyer becomes interested in the seller’s property. In this situation, the licensee is not permitted to recommend or suggest a price, negotiate on the customer’s behalf, inform the customer of their client’s bottom line price point or disclose any confidential information about their client unless otherwise authorized by the client. However, the licensee can provide a customer with other services, such as:

- explaining real estate terms, practices and forms;

- assist in screening or viewing properties;

- prepare and present all offers and counter offers at the customer’s direction;

- inform you of lenders and their policies; and

- identify and estimate costs involved in a transaction.

Services a Buyer Can Expect From a Real Estate Licensee

You can expect licensees to provide you with such services as:

- Helping you to clarify the type of home you need and can afford

- Providing information about available properties and sources of financing

- Arranging appointments to view available properties

- Providing accurate answers to any questions you may have about a specific home you are considering

- Explaining the forms used in a real estate transaction and assisting you in making a written offer to purchase

- Presenting your written offer to the seller

- Familiarizing you with the steps you must take to complete the purchase after the seller accepts your offer.

Keep in mind that if the licensee with whom you are working is the seller’s agent, any information you give to him or her must be passed on to the seller. It is in your best interest to discuss with that licensee only what you would discuss with the seller in person.

The Big Search

Now it’s time to begin your informed search for that “right” home. You have gathered all the information you need to make a rational decision rather than an emotional one, but it may not be easy! You, like everyone else, will probably want what you can’t afford. Try not to become discouraged. Every homeowner started somewhere and it is most likely that there is a place for you!

What Should You Look For?

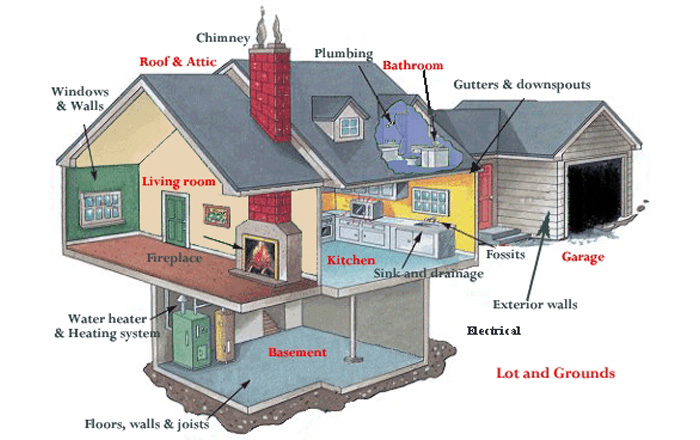

What Should You Look For?

After you have found a home, don’t be shy! You are about to invest a lot of money and you should investigate each home thoroughly. Pay particular attention to the following:

- What size and shape is the lot? Is it fully serviced with sewage, water, gas, and electrical lines?

- How many square feet of living space is there? How many rooms?

- Condition and age of the roof: Are there any leaks or recent repairs? If only part of the roof was repaired, will the rest cause trouble?

- Are there proper roof gutters and adequate downspouts which are properly connected to storm drains?

- Are the interior walls and ceilings solid? drywall or plaster? Is there any evidence of leaks or cracks?

- Are floors firm and level? What about the condition of the floor boards? and supports? Does the ceiling sag?

- Is there evidence of termites or dry rot?

- What types of floors are beneath the carpeting?

- Are stairs and door frames level and well joined? Is the natural lighting to your liking?

- Which way does the front face—north, south, east or west?

- Are the room sizes adequate for your family’s needs? Is the layout compatible with your habits?

- Is the kitchen suitable? Are there enough outlets and space for appliances? What about cabinets?

- Are storage areas and closet space adequate?

- Does it look like renovation work has been done? If so, are there copies of building, electrical and gas permits for this work? Plumbing work is covered by a building permit; however gas and electric work require separate permits.

- What is the condition of the electrical wiring? Are there cables visible in the basement or close to the electrical panel that are not fastened at regular intervals to the floor joists or walls? If so, that may be an indication that work was done on the electrical system without a permit.

- Is there a hot tub or swimming pool installed? If so, check for evidence that there are electrical permits for these installations—it is very important for you and your family’s safety that proper grounding of the electric systems for these devices is in place.

- Has a gas fireplace insert been added at some stage? Is there a gas permit for this installation? Proper clearances from combustibles for these installations are critical and evidence that a permit was taken out for this work is confirmation that the work was done by a licensed contractor and/or inspected by a qualified person.

- What about satisfactory ventilating equipment? Are there exhaust fans in the kitchen and bathrooms?

- What type of heating system is it (forced air, gravity, etc.)? What kind of fuel is used? Is there a heat pump?

- Is there sufficient electrical wiring? Is there enough power for your electrical equipment? Are there adequate outlets in the home? Has the fuse box been updated?

- Can the wall space be utilized to suit your needs? Check the locations of doors and windows.

- Drainage—is the home well drained and has landscaping been done to prevent erosion?

- What is the condition of the basement and foundation? You should check the walls and floors. Is the floor dry?

- Are there hookups for a washer and dryer?

- What about the attic or crawl space? Is there evidence of leaks? Dry rot? Is there proper ventilation and insulation? Does the insulation meet current specifications?

- Are there severe cracks in or excessive or uneven settlement of the foundation?

- How large is the garage? Is the driveway adequate? Is there cracking or lifting and is drainage satisfactory?

- What is the condition of caulking on windows and doors? What kind of storm windows are there and what condition are they in? Do windows and doors open and close easily?

Each home is unique. Keep some notes to enable you to remember the details later!

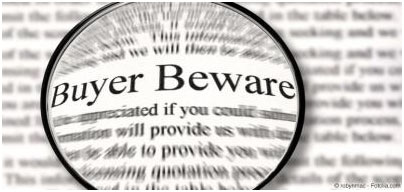

Buyer Beware!

If you think you have found the right home, but you have some concerns about its structural soundness, now is the time to call in an expert. Consider having the home inspected by a building inspection service which will prepare a written report. Your purchase is a big investment, so think of the fee for this service as an insurance premium.

Be aware that home inspections are primarily visual inspections and they may not reveal problems with electrical or gas systems. If there is evidence that there are some issues with the electrical or gas systems and/or work has been done without appropriate permits, you should consider having people with qualifications in those areas inspect those systems.

Stigmatized or Psychologically Impacted Properties

Sometimes when dealing in real estate, the onus will be on you, the buyer, to ask questions regarding issues of specific importance to you and your family, rather than relying on a real estate licensee to try to anticipate all of your needs.

If, as a potential buyer, you are concerned about the less obvious structural and mechanical aspects of a property, you can have a property inspection done. However, consumers may have other areas of concern that would cause them to avoid a property. Certain events may cause a property to be described as a “stigmatized property” or a “psychologically impacted property”. These terms are sometimes applied to a property that has had some circumstance occur in or near it, but which does not specifically affect the appearance or function of the property itself.

Examples of these in a residential context might include:

- a sexual offender is reported to live in the neighbourhood;

- a former resident was suspected of being an organized crime

- gang member;

- a death occurred in the property;

- the property was robbed or vandalized; and

- there are reports that the property is haunted.

British Columbia law does not define stigmatized properties. It also does not require sellers or licensees who represent them to disclose circumstances which some may be considered to be stigmas. Buyers are advised to carefully consider the areas of concern they have, discuss them with their licensee, and ensure the necessary inquiries are made to avoid purchasing a property they will not feel comfortable living in.

What Other Questions Should You Ask?

Is a Property Disclosure Statement available?

Is a Property Disclosure Statement available?

In British Columbia, sellers may have completed a Property Disclosure Statement. This statement provides information about the state of the home to potential buyers.

What is the Zoning on this Home?

The zoning on a home is established by the local government. Zoning sets the type of buildings which may be built on any particular piece of property and how those buildings may be used: single-family residential, duplexes, multi-family residential, commercial, or industrial. You may also wish to ask about the zoning on the surrounding properties to determine if, for instance, a factory or a park could suddenly appear nearby.

Is a Land Title Search Available?

A Land Title Search will allow you to see who is registered as the current owner of the home and if there are any registered mortgages, easements, restrictive covenants, rights of way, etc. which may affect the use or value of the home.

Are There any Restrictive Covenants?

A restrictive covenant places a specific limitation on the owner’s use or occupancy of the property. Such things as a prohibited type of exterior finish, the minimum size of the structure, or the maximum height of the structure are only a few examples of the type of restrictive covenants you may encounter. The act of purchasing a property which has a restrictive covenant compels you to abide by it.

Are There any Easements?

An easement is a right or privilege one party has to use the land of another for a special purpose. Examples are: easements given to telephone and electric companies to erect poles and run lines over private property, easements given to people to drive or walk across someone else’s land, and easements given to gas and water companies to run pipelines to serve their customers.

How Much are the Property Taxes?

As stated earlier, the amount of property taxes payable will figure in the calculation of how much money you can borrow to finance your purchase.

Is the Structure Covered by any Warranty?

Homes built by a licensed residential builder under a building permit applied for on or after July 1, 1999, or where construction began on or after July 1, 1999 in areas where no building permit is required, are subject to the mandatory third-party warranty insurance provisions of the Homeowner Protection Act, unless there is an applicable exemption. The licensee with whom you are working can assist with acquiring warranty information. The Homeowner Protection Office Branch of BC Housing (HPO) can assist with questions regarding warranty issues. The HPO can be reached through their toll-free information line at 1-800-407-7757 or you can refer to their web site at www.hpo.bc.ca.

Fixtures vs. Chattels

Things contained in a building or on the land are classified as either fixtures or chattels. The difference between a fixture and a chattel is very important to you because fixtures stay with the home when it is sold, but chattels depart with the old owner. If you see an attractive fireplace insert, a “murphy bed” in the spare bedroom closet, a vacuum canister in the utility, or custom window blinds which you think should stay, but are not certain if the seller agrees, ask if it is a fixture.

Are there permits in place?

Are there permits in place for building and/or renovation work and for the electrical and gas systems including original and alterations/additions? For information on what type of work in a home requires gas and electric permits, please contact the BC Safety Authority at 1-866-566-7233 or visit www.safetyauthority.ca.

What About Strata Properties and Cooperatives?

If you are contemplating the purchase of a home which involves the strata or cooperative type of ownership, there are some additional points to consider:

- What are the monthly charges for common area maintenance (strata fees)? What services or utilities are included?

- Does the building have a good reputation for honesty and successful operations? Are units not controlled by the developer being successfully resold?

- Who controls the recreational facilities? Will you be required to pay extra fees for using any of the facilities or amenities? If it is a new development, is there a certain date when your unit will be ready for occupancy? Will the swimming pool and recreation facilities be completed by that date?

- How is the property being managed? Is the property being managed by a company licensed by the Real Estate Council to provide strata management services or is it being “self managed” whereby the management is the responsibility of the owners collectively?

- How much money is in the contingency reserve fund and what portion of the strata fee is being contributed monthly to this fund? What capital expenditures (common expenses that usually occur less than once per year or do not usually occur) is this fund being maintained for (e.g. roof replacement, water piping replacement, interior decorating upgrades, etc.)?

- Are owners permitted to rent their units to tenants? How many rental units will be allowed in the project?

- Are pets allowed in the building? Are there any other restrictions on use?

- Have any special assessments been agreed upon or have any structural problems been noted which may lead to a special assessment in the future?

- Has the building envelope been renovated in the past? Since October 1, 2000, all contractors who engage in, arrange for, or manage building envelope renovations in British Columbia must be licensed as a building envelope renovator with the Homeowner Protection Office and must provide applicable third-party home warranty insurance on applicable building envelope renovations.

- What about parking stalls and storage lockers? There are two main designations of property in strata developments which can be found on a strata plan—those being property designated as either a strata lot or common property (CP). Common property can then be further designated as limited common property (LCP) for the exclusive use of one or more strata lots. The strata plan usually contains one or more of the following arrangements for parking stalls and storage lockers.

- the parking stall or storage locker is a separate strata lot. Although rare, parking stalls and storage lockers can exist as a separate strata lot with their own strata lot number. This designation can be identified by looking at the strata plan.

- the parking stall or storage locker is part of a strata lot unit. Parking stalls and storage lockers that are part of the strata lot will share the same strata lot number as the unit (the main strata lot) which uses the stall or locker. This designation allows the buyer to have automatic use of the stall or locker.

- the parking stall or storage locker is part of the common property. If the parking stall or storage locker is part of the common property, the strata corporation has ultimate control over the use of those areas, except in cases where there is a developer’s lease. Common property is owned by all owners as tenants in common. The strata council has the authority under the Strata Property Act to permit an owner to exclusively use common property.

If the parking stalls or storage lockers are designated common property, owners are entitled to use a particular area as a result of the strata council’s grant of exclusive use to that owner. This designation is handled by way of a short-term exclusive use agreement whereby the strata council allows the owner to exclusively use a particular parking stall or storage locker for a limited time period of one year. Although the strata council can renew the arrangement, it can also choose not to renew.

If the parking stalls or storage lockers are designated common property, owners are entitled to use a particular area as a result of the strata council’s grant of exclusive use to that owner. This designation is handled by way of a short-term exclusive use agreement whereby the strata council allows the owner to exclusively use a particular parking stall or storage locker for a limited time period of one year. Although the strata council can renew the arrangement, it can also choose not to renew.

In some strata developments, the developer has entered into a lease of the common property parking stalls and storage lockers to itself or to a company related to the developer. After leasing the common property, the developer then enters into agreements with buyers in which the developer subleases one or more parking stalls or storage lockers to each buyer. Often, the developer will assign one parking stall or storage locker to a buyer. These leases are seldom registered on title, which can make discovering them a challenge.

- the parking stall or storage locker is limited common property. Limited common property (LCP) is common property for the exclusive use of the owner of a particular strata lot. If the property is designated LCP, although it continues to be owned by all owners within the strata corporation as tenants in common, it may be used exclusively by the owner whose strata lot is identified on the strata plan as being entitled to use the LCP.

What information should you obtain about the building? Ask to see the registered bylaws, current rules, annual operating fund budget, Information Certificate (Form B prescribed under the Strata Property Act) and at least the last two-years’ minutes of all meetings (including strata council meetings, annual or special general meetings and meetings of the executive (or of the members) of any section in the strata corporation to which the strata lot belongs). You should also ask to see any applicable warranty information, envelope inspection reports or remediation reports, the registered strata plan and any amendments or resolutions dealing with the common property and any correspondence to owners from the strata council over the last twelve months. These documents will govern the manner in which your unit and the common areas may be used. They will also advise you of what has been going on in the building. Read these documents very carefully as they may reveal potential problems in the building.

Ancillary Services – Inspection and Additional Investigation Reports

You have a property on which you want to make an offer! In addition to the information and suggested areas of investigation that you have reviewed earlier in this brochure, you may consider engaging the services of experts to provide inspections and reports on important components of a property. These services may be engaged prior to you making an offer or, more commonly, you may make your offer subject to you receiving and being satisfied with applicable inspections or reports. The cost of commissioning any inspection or report will vary and should be factored into your overall purchasing budget.

The types of inspections and reports you may wish to obtain will depend on the type of property, e.g. detached house, strata titled unit, recreational; the mechanical and service components, and geographic location of the property. Below is a list of the more common inspections and reports that are available to buyers. The list is organized alphabetically, not by order of importance, as the degree of importance of a particular inspection or report will depend on the specific nature of the property.

- Appraisal Report: provides guidance to the value of a property and may be required by mortgage companies or obtained by buyers who want an estimate of the value of a property.

- Depreciation Report: helps strata corporations plan for future repair and maintenance costs and helps prospective buyers to understand what repairs will be required and the future costs to a strata corporation to undertake the repairs.

- Electrical Inspection: an inspection of the electrical system and components of a property which will identify the deficiencies, if any.

- Engineers Report: provides information on the integrity of any buildings and other aspects of the property.

- Environmental Report: assists in determining if there are any environmental problems or considerations with a property, including but not limited to asbestos, radon gas, underground oil storage tanks or riparian areas.

- Furnace and Chimney Inspection: assists in determining if the furnace and the chimney meet current safety and insurance standards.

- Gas Line Inspection: undertaken by a natural gas utility, determines the integrity of gas lines and if any improvements to the property have been built over the gas service lines requiring their relocation.

- Home Inspection: provides information on the physical condition of a property.

- Municipal Compliance Report: from the municipality provides information relating to (non)compliance with municipal bylaws and regulations, or to waivers granted by the municipality.

- Plumbing Inspection: an inspection of the plumbing and drainage components of a property outlining any deficiencies.

- Property Disclosure Statement: a statement provided by a seller concerning the condition of a property, to the best of their knowledge.

- Surveyors Certificate: a report showing the property boundaries and the location of all improvements in relationship to those boundaries.

- Septic/Sewer Inspection: determines the condition of the sewer/septic system.

- Title Search: ascertains the ownership of land and whether there are any easements, restrictive covenants, leases, mortgages and encumbrances and charges registered against the land.

- Water Quality/Quantity Test: determines the recovery rate and quality of the water supply.

- Wood Stove/Fireplace Inspection: undertaken to determine if the wood stove or fireplace meets insurance requirements.

You may request other inspections or reports concerning specific components of a property, such as the roof, air conditioner, or any other component where the condition of that component would be material to your decision to buy a property.

Making an Offer

Once you have found the home you would like, a written offer to purchase must be prepared. Considering the substantial nature of this investment, you should work with a lawyer, notary public, or a real estate licensee when preparing an offer to purchase. An offer is usually recorded on a standard form entitled Contract of Purchase and Sale.

What Should the Offer Contain?

When you prepare an offer, it should contain a number of standard details, plus any conditions which are important to you. Be fully aware that once you sign this document and the seller also signs it, a legally binding contract has been formed. Legally binding means both you and the seller will be bound by the terms of the contract and must each perform your respective obligations as stated within that contract. Either of you can go to court to compel the other to perform his or her part of the contract. Even if a contract contains subject clauses, it is legally binding as soon as both the buyer and the seller have signed the contract.

When you prepare an offer, it should contain a number of standard details, plus any conditions which are important to you. Be fully aware that once you sign this document and the seller also signs it, a legally binding contract has been formed. Legally binding means both you and the seller will be bound by the terms of the contract and must each perform your respective obligations as stated within that contract. Either of you can go to court to compel the other to perform his or her part of the contract. Even if a contract contains subject clauses, it is legally binding as soon as both the buyer and the seller have signed the contract.

Your offer should include:

- Date of offer. Date and time your offer expires.

- Full legal names and addresses of both the buyer and the seller.

- Full legal description of the home.

- Amount of the deposit you are giving (which will be held in a trust account and will form part of your down-payment).

- Sale price.

- Amount of your cash down-payment and details as to how you will finance the remainder of the purchase price. Your desired closing and possession dates.

- A list of the conditions which must be satisfied before the sale can occur. These are called “subject clauses” or “conditions precedent.”

- A list of items which are not attached to the building (chattels), but which you state are to be included in the sale price; for example, drapes, refrigerator, stove, etc. It is helpful to be specific in the description of these items. Your signature.

What are the Seller’s Options?

When the seller receives your “offer to purchase,” he or she has four options.

Accept the Offer Exactly as Written

If the seller signs your offer without making any changes, a legally binding contract has been formed. Again, legally binding means both you and the seller will be bound by the terms of the contract and must each perform your respective obligations as stated. Your performance can be enforced in a court of law.

Reject the Offer

The seller is under no obligation to accept your offer or to make a counter-offer.

Ignore the Offer

The seller is under no obligation to acknowledge receipt of your offer.

Make a Counter-Offer

If the seller changes anything at all on your original offer, the seller is considered to have rejected your offer and to be making a new offer back to you. This new offer is usually referred to as a “counter-offer.”

When you receive a counter-offer, you then have the same three options as the seller had: accept, reject or make a further counter-offer. The process of counter-offers may continue until an agreement is reached.

If the counter-offer is unacceptable to you or if you have changed your mind about the purchase, the seller does not have the option of returning to your original offer and accepting it.

What are the Buyer’s Options?

If, after making a written offer, you decide you don’t want to purchase the home, it may be possible to revoke the offer. Many legal problems can result from the revocation of an offer, so you should seek professional advice about the correct procedure to follow.

More About “Subject” Clauses

The purpose of a subject clause (also known as a condition precedent) contained in an offer to purchase is to set out a specific condition which must be fulfilled before the sale can go through, although the contract is legally binding once it is signed by both parties.

Subject clauses must be carefully and precisely worded. You would be wise to get professional help in composing them; however, it is ultimately your responsibility to be sure the clauses mean what you want them to mean.

There can be as many subject clauses as you are able to negotiate with the seller; however, the fewer you put into an offer, the more serious you seem as a buyer and the better the chance is that your offer will be accepted. Remember that you are, in effect, asking the seller to take the home off the market during the period while you are attempting to fulfill the conditions you have set.

Some possible items you might wish your purchase to be “subject” to include:

- a satisfactory professional building inspection

- the arrangement of the financing you require

- the lender’s approval of your application to assume the seller’s existing mortgage

- the sale of your present home

- if the home is a strata lot, satisfactory review of all relevant strata documentation, including engineer’s reports and/or building inspection reports, if any.

When you place “subject” clauses on your offer to purchase, you are required to use every reasonable effort to see that the conditions are satisfied. It is important to know that subject clauses are not “escape” clauses that allow you to avoid your legal responsibilities in the contract. Once you have fulfilled the conditions, written notification should be given to the seller that you are removing the subject clauses.

If you are unable to meet the conditions after making every reasonable effort to do so, the contract ends and there is no legal obligation to complete the purchase. It is important to remember that if the brokerage is holding your deposit, both you and the seller must sign a deposit release form prior to the deposit being released to you.

A seller may wish to accept your offer containing subject clauses, yet still be free to consider other offers until you have removed the conditions. To allow him or herself this freedom, the seller may ask for a clause in the agreement which permits the seller to require you to remove all subject conditions within a short, specified time period (usually between 24 and 72 hours) if the seller receives another attractive offer. If you cannot do so, your conditional contract comes to an end. Sellers are most likely to request this time clause where you have made an offer which is subject to the sale of your current home.

A seller may wish to accept your offer containing subject clauses, yet still be free to consider other offers until you have removed the conditions. To allow him or herself this freedom, the seller may ask for a clause in the agreement which permits the seller to require you to remove all subject conditions within a short, specified time period (usually between 24 and 72 hours) if the seller receives another attractive offer. If you cannot do so, your conditional contract comes to an end. Sellers are most likely to request this time clause where you have made an offer which is subject to the sale of your current home.

More About Deposits

Usually, you will make a deposit with your offer to purchase or after your offer is accepted. That deposit is usually held in your brokerage’s trust account. The brokerage holds the deposit for the benefit of the transaction, not just for your benefit. Note: If your contract contains subject clauses in your favour and you do not remove those clauses, you will not automatically get your deposit back. Both you and the seller will have to sign a separate release form. If the seller will not sign the release, you will have to obtain legal advice, as your brokerage cannot release the deposit unless you and the seller have agreed to do so.

Unless the contract specifically states that any interest earned on a deposit will be payable to either the seller or the buyer, interest is payable to the Real Estate Foundation of BC.

If a deposit is to be held by someone other than a real estate brokerage, you should obtain independent legal advice to ensure there is no concern about either how the deposit is to be held or the terms upon which it may be released.

Completing Your Purchase

The Contract of Purchase and Sale, which you signed, will state the completion day for the transaction. On that day, legal ownership will transfer from the old owner to you in exchange for the purchase price of the home. You will be able to move in on the possession date stated on your contract. The completion and possession dates are not necessarily on the same date.

Do You Need Legal Assistance to Complete the Purchase?

It is normal practice for the buyer to engage a lawyer or notary public to prepare the documents necessary to transfer the legal ownership. Among other things, he or she will protect your interests by:

- searching the title in the Land Title and Survey Authority Office registration system to find if anyone other than the seller has any legal rights to the home and to see if there are any registered easements or restrictive covenants

- preparing the documents to transfer ownership from the seller to you, including the Property Transfer Tax return

- ensuring that the seller’s old mortgage has been properly discharged, if this is required

- confirming that all payments for which the seller is responsible have been made

- arranging for you to sign the transfer documents

- preparing a Statement of Adjustments outlining all monies owed by you and the funds you will need to complete the transaction

- delivering the final amount due to the seller and ensuring you are registered as the owner in the Land Title and Survey Authority Office

- obtaining documents for strata titled properties, such as the Information Certificate (Form B as prescribed in the Strata Property Act), Certificate of Payment (Form F as prescribed under the Strata Property Act) and the strata corporation’s Certificate of Insurance

The day has arrived! You have signed the documents, turned over your cheque, and received the keys. The home is yours!

© https://www.recbc.ca/about/consumer/buyinghome.html