How the U.S. Federal Reserve rate hike might affect Canadians

Posted by Steve Harmer on Thursday, March 16th, 2017 at 11:09am.

The U.S. Federal Reserve raised its key interest rate from 0.75 per cent to 1 per cent today, in a move widely anticipated by economists and investors.

The U.S. Federal Reserve raised its key interest rate from 0.75 per cent to 1 per cent today, in a move widely anticipated by economists and investors.

The hike is the second increase since December and reflects growing confidence at the central bank that the U.S. economy is now on solid footing.

Meanwhile, Canada’s key interest rate has remained at 0.5 per cent since July of 2015. What does this mean for Canadians and their finances?

1. The spread between fixed-rate and variable-rate mortgages could grow wider

The Fed’s move could lead to higher interest rates for fixed-rates mortgages in Canada, but it won’t have an effect on variable-rate mortgages.

Traditionally, a hike in the U.S. benchmark interest rate will also push up long-term interest rates in Canada, raising borrowing costs for Canadian banks. The banks, in turn, will transfer some of those costs onto consumers, by adjusting their own interest rates, including those on new fixed-rate mortgages.

The interest rate on variable-rate mortgages, however, is normally pegged to the Bank of Canada’s policy rate, which isn’t expected to rise any time soon.

“Fixed-rate mortgages will likely rise 0.20 to 0.25 of a percentage point,” predicted James Laird, president of brokerage firm CanWise Financial and co-founder of RateHub, a rates-comparison website.

This could push the spread between 5-year fixed-rate mortgages and 5-years variable-rate mortgages beyond 1 percentage point, said Laird, a threshold beyond which there is generally a sizable increase in the number of Canadians who will opt for variable rates.

“Any consumer who can handle the increased risk exposure of a variable rate should have a serious look at it,” added Laird.

For Canadians who can’t afford or stomach the added risk of a variable rate, however, this could be bad news.

Higher fixed-rate mortgages would be “another challenge for first-time home buyers to enter the market after tighter federal mortgage rules were introduced last fall,” said Laird.

2. Little impact on the exchange rate or consumer prices

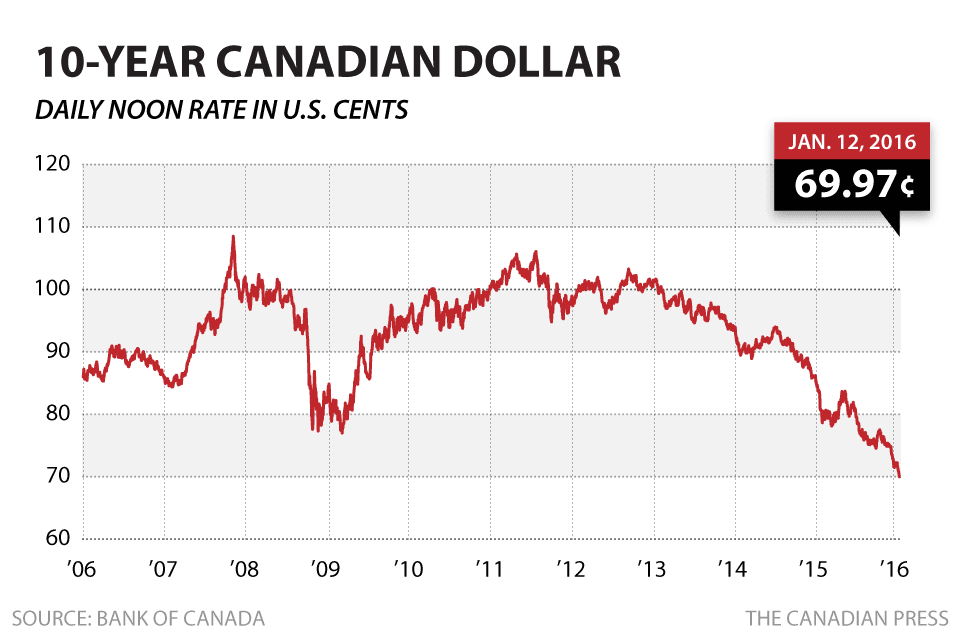

A widening spread between U.S. and Canadian short-term interest rates normally translates into a weaker loonie. Any impact on the Canadian dollar this time, however, is likely to be muted, said BMO chief economist Douglas Porter.

A widening spread between U.S. and Canadian short-term interest rates normally translates into a weaker loonie. Any impact on the Canadian dollar this time, however, is likely to be muted, said BMO chief economist Douglas Porter.

Today, the U.S. dollar actually weakened, likely because the Fed appeared a bit more cautious about the health of the U.S. economy than investors had expected. Meanwhile, the Canadian dollar strengthened, as oil prices bounced back from recent lows.

In the longer term, the loonie will likely continue to soften through the summer, before strengthening, said Porter.

In general, the loonie has been moving in a much narrower range lately, compared to the wild swings we saw last year, he noted.

Any movement in the exchange rate will likely be too little to affect consumer prices, added Porter. A weaker loonie makes U.S. imports more expensive, but businesses have been absorbing a lot of those costs, instead of transferring them onto consumers, he noted.

The loonie weakened by almost 30 per cent at one point since it was at parity with the U.S. dollar, but consumer prices in Canada barely budged, Porter noted.

3. Virtually no gain for savers

Though the interest rate hike might push up long-term interest rates on both sides of the border, it won’t have much of an effect on GICs, said Porter.

Canadian retirees and other net savers will have to wait for the Bank of Canada (BoC) to lift its own policy rate in order to see a perceptible increase in returns, he predicted.

Canadian retirees and other net savers will have to wait for the Bank of Canada (BoC) to lift its own policy rate in order to see a perceptible increase in returns, he predicted.

4. The era of rock-bottom interest rates may be over

Porter does not see the BoC raising interest rates in the short term. Governor Stephen Poloz has “gone out of its way to explain that our situation is different than the U.S.’s,” Porter told Global News.

For example, while the U.S. unemployment rate dipped to 4.7 per cent, Canada’s stands at 6.6 per cent.

But the Fed’s interest rate decision today does increase the chance that the BoC’s next move will be to raise, not lower, interest rates, Porter added.

That likely won’t happen until 2018, he said, but “rates are turning the corner and they will ultimately start to move off those historic lows.”

© http://globalnews.ca/news/3311667/how-the-u-s-federal-reserve-rate-hike-might-affect-canadians-wallets/