To rent or to buy? 8 questions Canadians should ask before taking the plunge

Posted by Steve Harmer on Sunday, May 22nd, 2016 at 10:27am.

Should you rent or buy?

Should you rent or buy?

Conventional wisdom suggests it’s a no-brainer – buying real estate is a worthwhile investment with a high return.

Despite record low interest rates, the sky high prices and carrying costs are causing many to rethink the allure of home ownership.

When you factor in the costs of repair, maintenance and other expenses associated with owning a home, Toronto-based financial planner Shannon Simmons argues that renting and putting saved money into another investment may earn more in the long run.

If you filled in a questionnaire asking where you see yourself in 10 years, many would answer “buying/owning a house. Do you really care if you buy a house, but think you should? Lets look at both sides of the argument and give a blanced view of the Rent-vs-Own debate.

Based on advice from financial planners—both independent and those employed by banks—Global News has compiled a list of questions (and some context) to help you decide whether buying or renting is the right move for you.

1) Do you have 10-20 per cent of the home’s purchase price saved for the down payment?

While it’s possible to purchase a home with as little as five per cent down in Canada, big banks prefer first-time home buyers to have an average of 10 per cent.

While it’s possible to purchase a home with as little as five per cent down in Canada, big banks prefer first-time home buyers to have an average of 10 per cent.

“If this is the property of your dreams and it’s a really good buy, and you don’t have the full 20 per cent down,” says Royal Bank of Canada’s Rachel Wihby, it may make sense to pay the mortgage loan insurance charged to anyone who doesn’t put 20 per cent or more down on the home.

But “the less you put down, the higher the amount that you’re actually being charged,” Simmons said. That could mean you end up paying an additional $10,000 or more.

2) Do you have another 1.5-5 per cent saved for closing costs?

First-time home buyers don’t have to pay realtor fees, but there’s a number of other closing costs that need to be taken into account.

Depending where you live, land transfer taxes can carry a “significant” price tag, said Farhaneh Haque, director of mortgage advice for TD Canada Trust. BC's current transfer tax is 1% on the first $200,000 and 2% on the balance, if you are a first time home buyer that is waived on your first purchase on a home up to a maximum of $450,000

Depending where you live, land transfer taxes can carry a “significant” price tag, said Farhaneh Haque, director of mortgage advice for TD Canada Trust. BC's current transfer tax is 1% on the first $200,000 and 2% on the balance, if you are a first time home buyer that is waived on your first purchase on a home up to a maximum of $450,000

“Lawyer fees, seller/buyer property tax adjustment, appraisal fees, home inspection fees, even just your moving costs,” Haque said.

David Stafford, Scotiabank’s managing director of real estate secured lending, added fire and loss insurance to the list, suggesting $50-$100 per month as a ballpark figure.

Stafford also stressed the value of a building inspection, particularly for first-time home buyers, who may be easily impressed by granite countertops and hardwood floors but miss such other details as an old furnace, a leaky roof, or electrical wiring that’s in need of repair.

“Given you’re contemplating a multi-hundred thousand dollar purchase, a building inspection for a couple hundred dollars isn’t a bad idea.”

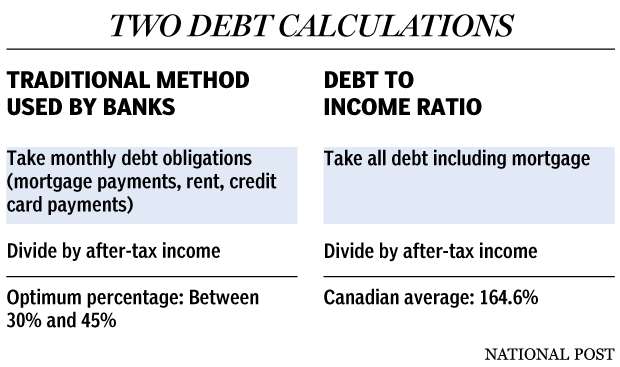

3) Can you keep debt servicing below 40 per cent of your income?

Your total debt service ratio measures the percentage of your gross annual income needed to cover housing payments (principal, interest, property taxes and heat, known as “PITH”) plus registered debts like car loans, personal loans and credit cards if applicable. Simmons says this 40 per cent rule is “specifically to please the bank” and is the general eligibility criteria when applying for your mortgage at most financial institutions.

So if you add it all up, housing payments and other debts should be between 35 and 40 per cent of your gross annual income.

4) Are your monthly fixed costs at 50-60 per cent of your after-tax income?

These “fixed costs” include housing and transportation, groceries, toiletries, and “everything you have to pay every month whether you like it or not,” Simmons said.

These “fixed costs” include housing and transportation, groceries, toiletries, and “everything you have to pay every month whether you like it or not,” Simmons said.

“When the money hits your bank account, if more than 60 per cent is tied up in things that you can’t get out of every single month, then you have no room after that for spending money which is not a fixed cost – things like going out for dinner, going out with friends, weddings, anything else that’s not just a bill.”

Keeping this ratio under control ensures you have enough money left over to keep saving, and avoid becoming “house poor.”

“Once you buy a house, it’s not like retirement’s done; you still have to save for other things,” Simmons added. “You also want to make sure that you have enough cash flow every single month that you don’t have to go into credit card debt – and that’s what I see: house broke, all the time.”

5) Can you save 1-2 per cent of your income in a “housing maintenance fee” each year?

The top mistake Canadian homebuyers make? Underestimating “significant renovations needed to the property,” according to a recent RBC poll.

Stafford suggests asking your realtor, and getting a home inspection.

Stafford suggests asking your realtor, and getting a home inspection.

“Even if it’s in pretty good shape, most homes of any age, there’s something you’ve got to do every year…and you need to factor that into your cash flows,” he said.

Simmons advises setting aside 1-2 per cent of your after-tax income each year to what she calls a “house maintenance fund” to avoid going into debt.

“When there’s not that extra cash sitting in an emergency fund, if there’s a $10,000 renovation or if you get cockroaches … It has to go on debt, because you’re not going to live in a place with cockroaches,” she said. “That can take a long time to pay off if you don’t have flexibility with your cash flow.”

6) Do you plan to stay in your home for at least three years?

Haque said TD advises clients to think about their life in three- to five-year chunks when considering purchasing a home.

A young couple buying a condo, for example, should consider how soon they’ll need a bigger space if they want children in the near future.

Wihby suggests regarding a home as a long-term investment – it might not be worth it if you buy a home and sell it a year later.

7) Is your job stable?

Are you planning to stay in your field? What would happen if your income decreased?

These are some of the questions RBC planners ask clients to determine how monthly payments and lifestyle would change as a result of job fluctuations.

“So you need to think of things like, will you be on a single income household instead of two?” Wihby said. “Maybe that means you won’t be taking those trips you thought you’d be taking or maybe you won’t be going to the gym as often.”

8) Are you emotionally ready to own a home?

It may sound hokey. But this is a big lifestyle leap to take.

It may sound hokey. But this is a big lifestyle leap to take.

“A lot of people heard that it was almost a no-brainer to go into property, especially when we saw property prices rising like we did in the past,” Wihby said. “But I think a lot of people got into purchasing a home before they were ready emotionally.”

The impact of what Stafford calls the “single biggest financial commitment for most people” includes the mental shock of going from a tenant to a homeowner.

“When you’re a tenant, the month that cheque goes out, it clears your account, and then you don’t think about it for the next 30 days,” Haque explained. “But when you’re a homeowner, you have those multiple payments like home insurance, maintenance fee, utilities, property taxes, that you have to account for on an ongoing basis. And sometimes it’s very much a shock to your system.”

“I know a lot of professionals who just don’t want to be bothered cutting the grass on Saturday, and doing the gardening. … They would much prefer to rent and save a bunch of money, so they can travel every weekend,” she said. “If you’re not actually going to enjoy the house, what’s the point in buying it?”

RENTAL INSECURITY

But, as anyone who has struggled to find a place to rent knows, renting isn’t a walk in the park either. Vacancy rates in the region hover at less than one per cent and have been on a downward trajectory since 2012, affected in part by the skyrocketing popularity of short-term rental platform Airbnb. Renting remains cheap relative to property values, but that doesn’t mean rentals are affordable. Rents are only expected to rise over time and there is already scarcity among certain types of rentals, such as three-bedroom units for families.

Final Word and other facts.

With BC's overheated real-estate market showing no signs of abating, many people are foregoing home ownership — at least for now — because the numbers simply don’t add up.

B.C. GOVERNMENT’S RENT-VS.-OWN CALCULATOR

A valuable number in real estate investing is the price to rent ratio, which is simply the purchase price dividend by the rent received. For example, the condo I purchased for $126,000 and rent for $1,300 / month would have a Price-Rent Ratio of 96.9 (monthly) or 8.08 (annualized).

One measure to determine whether it’s better to rent or to buy is a metric called the price-to-rent ratio, which takes the price of the property and divides it by its annual rent. Ratios in the 10-13 range indicate it’s better to buy than to rent, while a ratio in the 18-20 range is a sign in favour of renting over buying. Anything in between is a judgment call based on personal situation and local market conditions, according to Toronto-based BMO senior economist Robert Kavcic. Based on the recent figures for apartments, Vancouver’s price-to-rent ratio is 55 in the east of the city and a staggering 72 in the west side. This calculation doesn’t take into account other costs of home ownership, such as property taxes or maintenance and repairs.

Throughout most of the 20th century, renters have run the gamut of people in all socio-economic classes, said Andy Yan, an urban planner and acting director of Simon Fraser University’s City Program. Renting didn’t used to be just for those who couldn’t afford to buy. But since the Great Depression and the World Wars, governments in North America have promoted policies to support home ownership, said Yan. The American or Canadian dream of owning a home was used to stabilize the economy and ensure people have assets in their later years through the “forced” savings plan of a mortgage. “There’s a notion in Canada and the U.S. that rental is a temporary state only. But for an increasing population in places such as Vancouver and Toronto, it’s a housing reality,” Yan said, calling on government to recognize renting as a much-needed form of housing.

At the risk of over-simplifying, the rent-or-buy debate comes down to your values, what you prioritize in life, and what you can afford.

CLICK HERE TO TRY OUR FREE ONLINE HOME VALUATION TOOL

CLICK HERE TO TRY OUR FREE ONLINE HOME VALUATION TOOL

© http://globalnews.ca/news/985258/to-rent-or-to-buy-8-questions-canadians-should-ask-before-taking-the-plunge/