A mortgage is a huge undertaking

A mortgage is a huge undertaking

Just getting one sometimes can be hard. You have got your mortgage but did you look at the small print and read it? Here are some handy facts that you may not know.

- How much of your payments go toward interest

Most mortgage payments are what they call blended payments, which combine repayments of the principal as well as the interest at once. When you start paying off your mortgage, a significant part of your payments are going toward the interest, not the principal. Over time, however, the principal of your loan decreases, which means that the amount you will owe in interest decreases as well. As such, the portion of your payment that goes toward the interest will decrease over time, and the amount that goes toward the principal increases over time. This is why additional lump sum payments make such a big difference when it comes to your mortgage; they go directly toward your principal, whereas your usual mortgage payments do not. Use a mortgage calculator to determine how much you’ll end up paying in interest over the life of your loan.

- Your current lender won’t always give you the best deal at renewal

Most homeowners renew their mortgage with the same lender that holds their current mortgage. No problem there – except that more than half of homeowners renewed their mortgages without negotiating different terms than what was presented to them in their renewal statement, according to a 2015 mortgage consumer survey. Lenders are betting on the fact that you won’t want to switch lenders, and therefore aren’t bending over backwards to try and keep you. That means that you can probably find better rates and/or more flexible terms elsewhere. Don’t feel like shopping around? Call your mortgage broker to do it for you. Whether or not you used one for buying your home doesn’t mean that you can’t use them for refinancing.

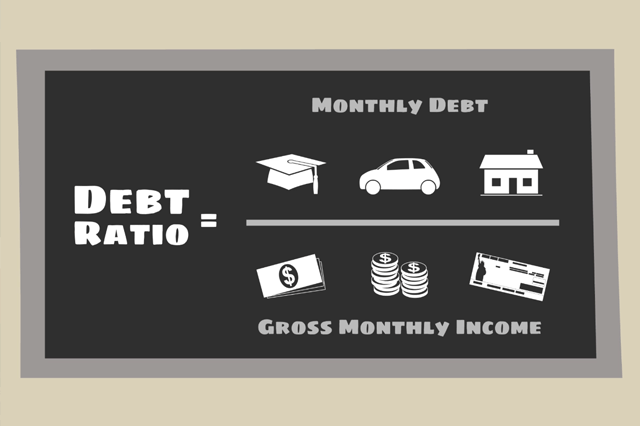

- Lenders want your monthly housing costs to be less than 32 per cent of your income

When your lender qualifies you for your mortgage, they use a system based on your reported and provable income as well as your debts. They want to ensure that your monthly housing costs – including your mortgage, property taxes, heating, and condo fees, if applicable – don’t use more than 30-32 per cent of what you’re bringing in. While this number is somewhat arbitrary and housing costs, incomes, and living expenses vary from one housing market to the next, if you don’t meet the criteria, then your mortgage application could be denied.

- A mortgage doesn’t equal a guaranteed good investment

A home is a big investment, and if you have a large mortgage, most of your net worth is tied up in one place. As any good financial planner will tell you, having all of your eggs in one basket isn’t a good long-term investment strategy; it’s the opposite of diversification. Still, everyone needs a place to live and if all goes well, you’ll end up with equity in your home, although you shouldn’t assume that you’ll be able to sell your home and cash in whenever you want to. Housing markets are cyclical, and the ups and downs can take decades to weather. If you want to buy a home, buy it because it fits into your overall long-term financial strategy, not because you want to retire in five years and need the income from the sale of your house.

- Missing a mortgage payment doesn’t automatically mean foreclosure

It’s pretty obvious that missing a mortgage payment isn’t a good thing. But life is full of unexpected surprises, and if you find yourself in a situation where you can’t come up with your mortgage payment one month, don’t throw your hands in the air and wait for the bank to issue an eviction notice. Foreclosure proceedings are a lengthy process, and everyone – your lender included – wants to avoid them if at all possible. So if you know you’re going to miss a mortgage payment, or if you already have, pick up the phone and call your lender. You may be able to negotiate with them and figure out a new or interim payment plan to get you back on your feel, or maybe an early refinancing in order to lower your monthly payments.

It’s pretty obvious that missing a mortgage payment isn’t a good thing. But life is full of unexpected surprises, and if you find yourself in a situation where you can’t come up with your mortgage payment one month, don’t throw your hands in the air and wait for the bank to issue an eviction notice. Foreclosure proceedings are a lengthy process, and everyone – your lender included – wants to avoid them if at all possible. So if you know you’re going to miss a mortgage payment, or if you already have, pick up the phone and call your lender. You may be able to negotiate with them and figure out a new or interim payment plan to get you back on your feel, or maybe an early refinancing in order to lower your monthly payments.

- Mortgage insurance can protects you as well as the lender

If you have a high-ratio mortgage, which means that you have a down payment of less than 20 percent, then you are required to get mortgage insurance, which protects your lender in the case you default on your mortgage. But the three main providers of mortgage insurance also have programs in place that homeowners can take advantage of if they fall into trouble. Genworth Canada has a Homeowner Assistance Program that is designed to help homeowners who are experiencing temporary financial difficulties work with the insurer to establish alternative arrangements to help homeowners stay in their homes. Canada Guaranty has a Homeownership Solutions Program, in which a member of their Loss Management team provides support to the lender in finding ways for borrowers to keep their homes, including enacting solutions such as reducing the contract interest rate to reflect current interest rates if it’s lower, extending the current mortgage term and/or extending the amortization period. Canada Mortgage and Housing Corporation (CMHC) provides tools to find a solution to  your financial situation, including converting a variable interest rate mortgage to a fixed interest rate mortgage in order to protect you from a sudden interest rate increase, should one occur, offering a temporary short-term payment deferral, adding any missed payments to the mortgage balance and spreading them over the remaining mortgage repayment period, and other alternatives to resolve or avoid mortgage payment default.

your financial situation, including converting a variable interest rate mortgage to a fixed interest rate mortgage in order to protect you from a sudden interest rate increase, should one occur, offering a temporary short-term payment deferral, adding any missed payments to the mortgage balance and spreading them over the remaining mortgage repayment period, and other alternatives to resolve or avoid mortgage payment default.

- You can get longer terms than 5 years

The 5-year fixed rate mortgage is one of the most popular products in Canada, but it’s not the only game in town. If you like having the certainty of a fixed mortgage payment, then you want to keep that certainty for as long as possible. Generally speaking, the longer the mortgage term, the higher the interest rate, but if you expect interest rates to rise in the next several years – which, rates being at a historical low, they almost certainly will – then you may be willing to pay for that certainty. Terms exist for up to 25 years.

© http://www.whichmortgage.ca/article/7-things-you-dont-know-about-mortgages-213995.aspx

Posted by Steve Harmer on

Leave A Comment