Your credit scores are an important aspect of your financial profile.

Your credit scores are an important aspect of your financial profile.

They may be used to determine some of the most important financial factors in your life, such as whether you’ll be able to lease a vehicle, qualify for a mortgage or even land that cool new job.

And considering 71 percent of Canadian families carry debt in some form (think mortgages, car loans, lines of credit, personal loans or student debt), good credit health should be a part of your current and future plans. High, low, positive, negative – there’s more to your scores than you might think. And depending on where your numbers fall, your lending and credit options will vary. So what is a good credit score? What about a great one? Let’s take a look at the numbers.

In a Nutshell

In Canada, your credit scores generally range from 300 to 900. The higher the score, the better. If you have scores between 800 and 900, you’re in excellent shape.

How your credit scores are set

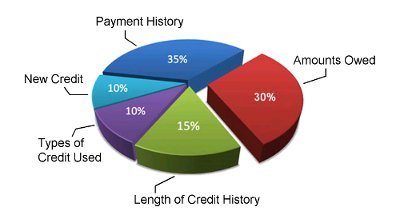

Canadian credit scores are officially calculated by two major credit bureaus: Equifax and TransUnion.

They use the information in your credit file to calculate your scores. Factors that are used to calculate your scores include your payment history, how much debt you have and how long you’ve been using credit.

Tip: You can view sample credit scores summaries from each bureau (see Equifax here and TransUnion here) to get a sense of what to expect.

What’s in a number?

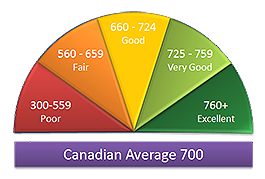

In Canada, your credit scores generally range from 300 to 900. The higher the score, the better. High scores may indicate that you’re less likely to default on your repayments if you take out a loan. Below you’ll see a general breakdown of credit score ranges and what each range means in terms of your general ability to qualify for lending or credit requests, such as a loan or mortgage.

Note that the ranges can vary slightly depending on the provider, but these are the credit score ranges you’ll see the most common agencies. The best way to know where your scores stand is to check your credit report:

Note that the ranges can vary slightly depending on the provider, but these are the credit score ranges you’ll see the most common agencies. The best way to know where your scores stand is to check your credit report:

● 800 to 900: Congratulations! You have excellent credit. Keep reaching for the stars.

● 720 to 799: You have very good credit! You should expect to have a variety of credit choices to choose from, so continue your healthy financial habits.

● 650 to 719: This is considered good to lenders. You may not qualify for the lowest interest rates available, but keep your credit history strong to help build your credit health.

● 600 to 649: This is fair credit. History of debt repayment will be important to demonstrate your solid sense of financial responsibility.

● 300 to 599: Your credit needs some work. Keep reading for some improvement suggestions below.

How to go from good to great (or bad to good)

To borrow from Joe Blow, all great credit scores are alike, but all bad credit scores are bad in their own way. That is, ideal credit scores are built on a similar set of healthy financial habits, but your scores can be damaged by any number of factors. There are many different issues that can hurt your credit, such as:

● Late or missed payments.

● Too many (or too few) open credit accounts.

● High credit card balances.

● High balances on loans.

● Too many credit applications.

The first step toward improving your credit health is avoiding getting trapped in the highs and lows of managing your credit.

Heather Battison, vice president of TransUnion Canada explains how consistency is key: “The most important factor for building and maintaining your scores is to pay your bills on time and in full each month. This activity demonstrates your ability to responsibly manage credit and can positively impact your credit scores.”

It’s also key to remember that your payment history isn’t just about paying your credit card bill. “It also includes things like your cellphone bill,” says Trevor Gillis, associate vice president of account management at TD Credit Cards.

Gillis says building good credit scores is “based on using your credit card responsibly, which means making at least the required monthly minimum payment (if you can’t pay off the balance in full), making your payments by the payment due date and keeping your credit card utilization low.”

Beware of third-party companies that claim they can quickly boost your scores. According to the Office of Consumer Affairs, only your creditors are able to alter the information on your credit file. When it comes to building good credit, there are no shortcuts.

Here’s the good-to-great news: Improving your credit health isn’t only achievable, but also the steps involved can help you establish an overall healthy financial life. Read our tips for everyday ways you can improve your credit health.

Bottom line

Help keep your credit scores as healthy as possible by reviewing your credit reports regularly to ensure they’re accurate. Making the decision to apply for a loan or credit card is a big deal – don’t let surprise scores get in the way of it.

There are ways to check your credit scores directly from TransUnion and Equifax. However, you’ll either be waiting for snail mail delivery (with the added risk of loss or theft in transit), or paying a fee for one-time online access (or a recurring cost for continued access).

© https://www.creditkarma.ca/credit/i/what-is-a-good-credit-score/

Posted by Steve Harmer on

Leave A Comment