New Mortgage Rules in 2018: Everything You Should Know

Posted by Steve Harmer on Monday, January 29th, 2018 at 11:12am.

What Are the Three New Mortgage Rules That Arrived In January 2018?

What Are the Three New Mortgage Rules That Arrived In January 2018?

New rules by Canada’s federal financial regulator announced in October 2017 mean that even borrowers with a down payment of 20 per cent or more will now face a stress test, as has been the case since January of 2017, for applicants with smaller down payments who require mortgage insurance.

Ottawa has already moved to tighten the rules around the mortgage market six times since July 2008, with a series of regulatory tweaks aimed at limiting the amount of debt that Canadians and financial institutions take on.

This is the seventh turn of the screw — and it could have a big impact. Some 10 per cent of Canadians who got an uninsured mortgage between mid-2016 and mid-2017 would not have qualified under the new standards, a recent analysis by the Bank of Canada suggested.

To put a number on it, the rules will likely affect about 100,000 home buyers, who would qualify for a mortgage for their preferred house today but will likely fail the stress test for an equally large loan next year, according a report published by Mortgage Professionals Canada, an industry group.

So what are the changes? Here’s how the new guidelines might affect you:

1. Stress Test

Starting on January 1, 2018, the Office of the Superintendent of Financial Institutions (OSFI) has set a new minimum qualifying rate, or “stress test” for all prospective home buyers, even those with a down payment of over 20%.

Before the new, tougher rule, only buyers that had a down payment of less than 20% had to make sure they could pass a stress test. Regardless of how much money you save for a down payment, if you don’t pass the new stress test, the bank won’t give you a mortgage.

Under the new mortgage stress test, potential home buyers need to qualify for a mortgage at a rate that is the greater of two indicators: either 200 basis points (2%) higher than the mortgage rate they qualified for, or the Bank of Canada’s five-year benchmark rate.

Before the new stress test, home buyers or owners qualified at the rate offered by the lender. The actual mortgage payment will still be paid at the negotiated rate, but a higher calculation is used for qualifying purposes.

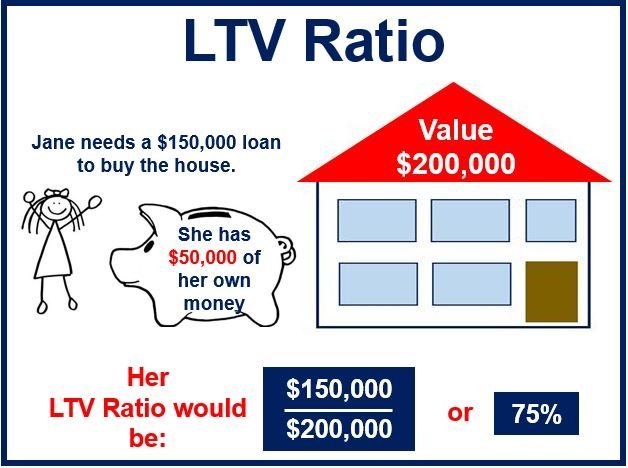

2. Enhanced Loan-To-Value Measurements

Traditional mortgage lenders (Canada’s big banks) need to ensure the Loan-To-Value (LTV) ratio remains “dynamic.” That means, it needs to be adjusted to local market conditions.

Traditional mortgage lenders (Canada’s big banks) need to ensure the Loan-To-Value (LTV) ratio remains “dynamic.” That means, it needs to be adjusted to local market conditions.

The OSFI insists that lenders (excluding private lenders) have internal risk management protocols in higher priced markets, like Toronto and Vancouver. A LTV ratio is a number that describes the size of a loan compared to the value of the property.

Canada’s big banks use the LTV ratio to determine how risky a loan is; the higher the LTV ratio the greater the risk.

For example, if property values decrease following a housing bubble, the LTV ratio could actually rise and be higher than the total value of the property. In which case, it’s quite possible that you have negative equity in the house.

3. Restrictions Placed on Certain Arrangements to Avoid LTV Limits

Mortgage lenders (again, this does not include private lenders) are not allowed to arrange a mortgage or other financial product with another lender that gets around the maximum LTV ratio or other limits placed on residential mortgages.

If you apply for a mortgage with a LTV ratio of 80% and the lender can only approve you for 60%, in the past, the lender couldpartner with a second lender for the additional 20%, bundle it together to get a complete LTV loan of 80%.

Traditional lenders cannot do this anymore.

What Does This Mean for Home buyers and Sellers?

The three new mortgage rules that kick in as of January 1, 2018 will hurt the fastest growing segment of Canada’s mortgage market—uninsured mortgages. That’s one out of every six prospective in the country. The strict stress test, which is meant to ensure borrowers can afford to pay their mortgage at a higher rate, is now being applied to all home buyers, even those with a down payment of 20% or more. Once the tests are in place, it is estimated that it could lower a family’s purchasing power by up to 21%.

The three new mortgage rules that kick in as of January 1, 2018 will hurt the fastest growing segment of Canada’s mortgage market—uninsured mortgages. That’s one out of every six prospective in the country. The strict stress test, which is meant to ensure borrowers can afford to pay their mortgage at a higher rate, is now being applied to all home buyers, even those with a down payment of 20% or more. Once the tests are in place, it is estimated that it could lower a family’s purchasing power by up to 21%.

Economists say the stricter mortgage rules will also negatively impact softening housing markets across the country. It is expected the tougher mortgage rules, once fully implemented, will depress housing demand by up to 10%. If you’re a home buyer and want to refinance a mortgage, the new mortgage lending rules will be a lot more difficult to negotiate.

Case 1. If you’re planning to buy a house with a downpayment of 20 per cent or more next year

The stress test means that financial institutions will vet your mortgage application by using a minimum qualifying rate equal to the greater of the Bank of Canada’s five-year benchmark rate (currently 4.99 per cent) or their contractual rate plus two percentage points.

If you’re going be house-hunting next year, this may force you to settle for a less expensive home than you would be able to buy today. Or, you might have to wait and save up for a larger down payment.

The rules might force Canadians to set their eyes on homes that are up to 20 per cent cheaper. But since few homebuyers are stretching their finances to the limit when applying for a mortgage, the average target price reduction will likely be smaller, $31,000, or 6.8 per cent, according to Will Dunning, chief economist at Mortgage Professionals Canada.

Of the 100,000 or so prospective home buyers that will hit a snag because of the stress test next year, Dunning estimates that about half will be able to make a different purchase than they had planned. The rest will give up on a home purchase.

Of the 100,000 or so prospective home buyers that will hit a snag because of the stress test next year, Dunning estimates that about half will be able to make a different purchase than they had planned. The rest will give up on a home purchase.

Case 2. If you’re renewing your mortgage next year

Lenders don’t have to apply the stress test to clients renewing an existing mortgage.

This means that if you fail the stress test, you’ll probably get stuck renewing with your current financial institution, without being able to shop around for a better rate.

In some cases, “renewing borrowers may be forced to accept uncompetitive rates from their current lenders,” Dunning noted.

Case 3. If you’re refinancing your mortgage

If you’re planning on refinancing your mortgage, you’ll have to qualify according to the higher stress-state rates rather than your existing contractual mortgage rate, explained James Laird, president at Toronto-based CanWise Financial.

Say, for example, that you bought a $400,000 home and have a $100,000 mortgage balance left. You’d like to borrow $50,000 more for a renovation. You have a five year fixed-rate mortgage at 3.3 per cent.

Today, your lender would make sure that you can take on a $150,000 loan at 3.3 per cent, said Laird.

Starting next year, your financial institution would have to vet that $150,000 loan using a 5.3 per cent rate. If you’re close to the borrowing limit today, you might have to settle for a smaller loan.

READ MORE - See our blog articles on mortgages

Cases in which the rules likely won’t affect you

As they generally do, financial regulators have allowed for measures that will ease the transition, making sure the new rules don’t disrupt transactions that are underway by not yet completed in early 2018.

If you have signed a purchase agreement on a new home before Jan. 1., lenders won’t have to apply the stress test even if you apply for a mortgage in the new year, said Laird. This holds for pre-construction sale and purchase agreements, too, he added. “Usually there’s eventually a cutoff,” said Laird, though in this case it’s not yet clear when that will be.

If you are pre-approved for a mortgage, some lenders will give you 120 days starting Jan. 1 to buy your new home without worrying about the new rules.

The same holds for mortgage refinancing. If you had a mortgage refinance commitment in place by Dec. 31, you have 120 days to follow suit, said Laird.

Of course, the stress test won’t have much of a concrete impact on you if you pass it. Borrowers with plenty of spare financial capacity will be able to go about their business.

About credit unions

The Office of the Superintendent of Financial Institutions (OSFI) rules only apply to federally regulated financial institutions, meaning Canadians might be able to continue borrowing without a stress test if they turn to provincially-regulated credit unions.

In the past, however, credit unions have voluntarily adopted new federal standards on mortgage rates “pretty quickly,” said Laird. Still, adopting rules on a voluntary basis means they would be able to make some exceptions, he added.

The stress test measures only one of three risk metrics lenders look at, said Laird. Essentially, it ensures that borrowers’ housing expenses compared to their income remain below a certain threshold even if rates rise. But when evaluating a borrower, financial institutions also look at the size of the loan compared to the price of the house, as well as credit scores.

A credit union that has voluntarily adopted the stress test, might make an exception for a family with very strong credit scores and a down payment considerably higher than 20 per cent, even if they fail to qualify under the new rules by a small margin, said Laird.

A credit union that has voluntarily adopted the stress test, might make an exception for a family with very strong credit scores and a down payment considerably higher than 20 per cent, even if they fail to qualify under the new rules by a small margin, said Laird.

Should You Be Worried?

If you’re a first-time home buyer, the stricter mortgage lending rules mean you might need to rent for a little longer or wait until your income increases before you can buy a home.

Because the purchasing power does not go as far as it once did, first-time home buyers might need to consider something besides a detached house—a townhouse house or a condo. Or, first-time home buyers may need to get a co-signer to qualify under the strict new rules.

There are other options though. Keep in mind, the stricter mortgage lending rules only apply to those home buyers looking to secure a mortgage with one of Canada’s federally regulated mortgage lenders.

Canada’s new mortgage rules are going to make it a lot more difficult for potential home buyers to secure a mortgage. But you shouldn’t let the new mortgage rules prevent you from getting the mortgage you deserve.

Make sure as always you take good advice from Professionals.