The Step by Step Plan to Buying Your First House in 5 Years

Posted by Steve Harmer on Thursday, January 30th, 2020 at 2:42pm.

Buying your first house can feel overwhelming, but it’s oh-so-worth-it to leave the rental life behind.

Buying your first house can feel overwhelming, but it’s oh-so-worth-it to leave the rental life behind.

We break down the process for you to help get you on the right path to living in your dream home.

1. Save, save, save

First things first: You need to start a savings fund for your home purchase. “Home buyers should have at least 10 percent of the purchase price of the home in their savings account,” says Randall Yates, CEO, The Lenders Network. “In addition, lenders like to see at least two to three months’ worth of mortgage payments in reserves.”

There are also different types of mortgage programs available for new or low-income buyers that require a lower down payment, so be sure to research your qualifications for these programs while socking away the savings.

2. Check your credit score

Doing so early into your home buying process gives you plenty of time to improve your score and fix any negative marks. A credit score over 740 is considered the ideal range for mortgages. A lower score won’t disqualify you for loan approval, but it can mean a higher annual percentage rate (APR)—and the lower your mortgage rate, the lower your monthly mortgage payment and overall amount of your home loan.

3. Improve your credit score

If your credit score is not at the 740 mark, you can take steps now to dramatically increase it in 6 to 12 months. Together, payment history and the amount of money you owe make up 65 percent of your credit score. Make sure you consistently pay your bills on time and take steps to pay down your credit card debt to gain a healthier credit score.

Next, dispute any false information or negative marks on your report. “Some creditors are willing to, if you are currently up to date [with payments], remove late payment history,” says Deborah Spence, a Pennsylvania-based real estate agent. You can also close accounts that you don’t use anymore, like that credit card you used in college and have since forgot all about. Note: If you plan on applying for a mortgage within six months, leave the card open, as a recently closed card could ding your score.

4. Find a mortgage broker

A good mortgage broker will help you find the best rate for your loan and also help you sail through the process. Even though picking a good broker is crucial, only one-third of home buyers comparison shop for the best mortgage deal. It’s always smart to check with a national bank, a local one, and a credit union to learn about your different financing options.

Ask friends, family members, and your real estate agent for broker referrals. Be sure to read online reviews as well, and don’t be afraid to ask potential brokers all the questions you have and to see things in writing.

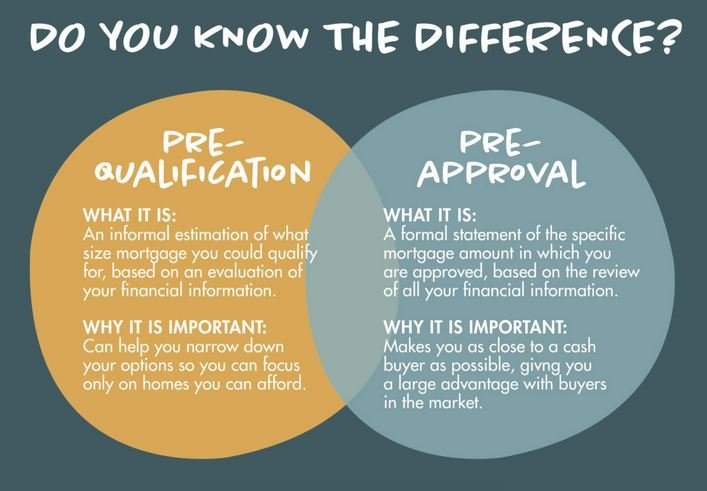

5. Pre-qualify for a mortgage

Getting pre-qualified for a loan will help you understand how much you can afford and even lock in a low-interest rate. “Buyers who have their lender letter in hand to provide to the sellers along with their offer will generally be in a much stronger position to make a successful bid,” explains Keith Hickman, a realtor in Los Angeles. This is especially important if you live in a competitive home market where you might be competing against other buyers for the same home. Pre-qualifications are generally good for 90 days, so you may want to wait until you’re fully ready to house hunt.

Getting pre-qualified for a loan will help you understand how much you can afford and even lock in a low-interest rate. “Buyers who have their lender letter in hand to provide to the sellers along with their offer will generally be in a much stronger position to make a successful bid,” explains Keith Hickman, a realtor in Los Angeles. This is especially important if you live in a competitive home market where you might be competing against other buyers for the same home. Pre-qualifications are generally good for 90 days, so you may want to wait until you’re fully ready to house hunt.

6. Keep your financial stats steady

Once you start the home buying process, you need to keep your financial health in check. Don’t make any major purchases, like thousands of dollars of new furniture, or open up another line of credit, like taking out a car loan.

This is also not the time to change jobs, quit, or switch to part-time hours. “Avoid changing jobs at all costs during the mortgage application process. It makes it so much more difficult and can impact how much you are paying for years,” warns Jordan Linville, the CEO of BrightRates, a website that allows consumers to compare interest rates.

7. Make a home wish list

Now it is time for the fun part—writing down your top desirables in your future home. This list can help save you time in the search process because your realtor can be more selective about which houses he or she shows you.

When making your list, don’t think only about immediate needs and wants. Consider what your life might look like five years into the future. Do you want to grow your household or do you have older children that will be going away to college? Look for homes that fit your current needs as well as your near future ones.

8. Find a great realtor

Whether you're buying or selling a property, a quality real estate agent is vital to make the process run smoothly. Seek out an agent with excellent credentials and references. Meet with a handful of agents to make sure any questions you have are answered. Watch out for potential red flags. Agents who charge very low costs or only work part-time may not be reliable.

© https://www.rd.com/home/buying-your-first-house/