What to do with a Low Home Appraisal

Posted by Steve Harmer on Monday, January 9th, 2017 at 12:30pm.

Low Home Appraisal - What now?

Low Home Appraisal - What now?

In the home-buying process, there are several crucial steps along the way that Sellers and Buyers alike will have to navigate: the home inspection, title issues, getting a survey and negotiating when an appraisal comes in significantly lower than the accepted offer.

When this happens both sides can go through many different emotions.

Either you, as the Seller, will feel as though you paid more than the property’s worth, especially if you just recently completed renovations, or, if you’re the Buyer, and you don’t have extra cash to hand over, the deal can fall apart. (Your lender’s not going to spring for a higher loan amount if the appraisal came in lower than expected, so Buyers will have to make up that difference themselves.)

Appraisers typically look at the last six months of sales in a comparable area. If sales were lower six months ago then that will affect the current appraisal, even if the market today is moving quickly and inventory is low.

If sales were higher six months ago, however, then the reverse will happen: appraisals can’t keep up with how quickly homes are selling in a hot market, so lower-than-expected values can be placed on homes.

So what are some things to think about in response?

So what are some things to think about in response?

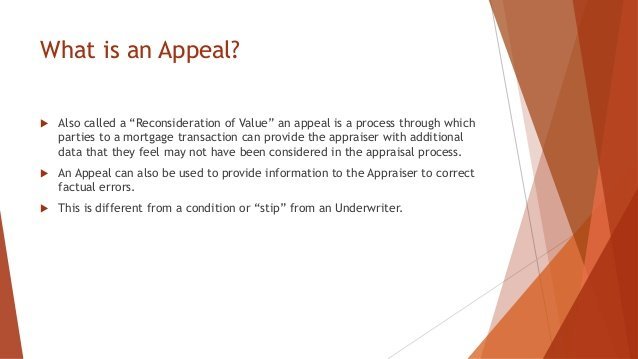

1. Appeal the appraisal

Sometimes called a “rebuttal of value,” the appraisal appeal takes some work. In fact, it’s a total team effort.

The Seller, lender and listing agent can work together to find better comps to justify a higher valuation – looking for anything that helps the claim. Perhaps the appraiser overlooked some comps (homes similar in style, location, and square footage sold within the past few years).

The mortgage broker/bank lending officer writes an appeal using the new comps and then sends it to the appraiser. There might be some negotiating back and forth until all parties come to a compromise with a new valuation.

This doesn’t always work, but it’s worth trying as many appraisers, if they’re given good solid information, may be willing to adjust their values.

2. Order a second appraisal

If the appraised value is not as high as the agreed upon contract sales price, the agent will ask to see the comps and ask to get a second or third appraisal to compare.

If the appraised value is not as high as the agreed upon contract sales price, the agent will ask to see the comps and ask to get a second or third appraisal to compare.

This is at the Buyer’s cost, however, so it’s a good idea to make sure your agent has a good solid reason to ask for a second opinion.

A Buyer is not only paying for the first appraisal (in the closing costs), but a second or third appraisal can range between a few hundred dollars and $1,000 depending on the area. Occasionally, real estate agents or Sellers will foot the bill if they really want to keep the sale.

3. Negotiate with the Seller

If you’re lucky, you and the Seller will both budge a little.

In writing up a contract, an agent will often insert an appraisal clause stating that if the house doesn’t appraise then the Seller and Buyer can reserve the right to renegotiate a new sales price or terminate the contract.

Often, the Buyer will go back to the Seller and ask them to reduce the price or split the difference. Sellers can decide if they want to do so, even though they’re under no obligation to, but they may prefer to do this rather than take a chance of losing you as a Buyer, and starting over again. Another Buyer might have the same issue, so the Seller might be better off renegotiating with you unless they have other offers.

Often, the Buyer will go back to the Seller and ask them to reduce the price or split the difference. Sellers can decide if they want to do so, even though they’re under no obligation to, but they may prefer to do this rather than take a chance of losing you as a Buyer, and starting over again. Another Buyer might have the same issue, so the Seller might be better off renegotiating with you unless they have other offers.

Lenders often require the use of their own approved appraiser, and these appraisals are “locked in” for six months.

A Seller will usually be upset about a low appraisal value, but most reasonable ones eventually come to terms with the fact that any other appraisal values by potential future Buyers will most likely come in at about the same value.

4. Walk away

No one wants to let a property slip through their fingers, especially if it feels like their dream home, but ignoring a low appraisal could end up losing you thousands whenever you decide to sell in later years, unless you’re truly in a hot up and coming market.

If you have an appraisal contingency in your contract, you can walk away, get your deposit back, and hope for better luck the next time around.

© https://www.charlottesvillesolutions.com/about-charles-mcdonald/