Why more Canadians are raiding their RRSPs

Why more Canadians are raiding their RRSPs

For the past 22 years, the Home Buyers’ Plan has helped more than 2.5 million Canadians borrow money from their RRSPs to help make the dream of home ownership a reality. However, the $25,000 maximum that can be withdrawn per person doesn’t give prospective homeowners a lot to work with.

The reasoning behind this plan is fairly straightforward. First-time home buyers (or anyone who hasn’t owned his or her primary residence in the past five years), are permitted to take up to $25,000 from their retirement savings without penalty as long as it is paid back within 15 years, which starts two years after the withdrawal occurs.

If you are buying with your spouse or common-law partner, it is possible to withdraw

With a credit score under 600, it is likely that you will be turned down by a bad credit or prime lender and you may have to turn to a private lender. Private lenders provide an option to clients with bruised credit. Since it is a fast financing option with a higher risk to the lender, interest rates are almost always higher.

With a credit score under 600, it is likely that you will be turned down by a bad credit or prime lender and you may have to turn to a private lender. Private lenders provide an option to clients with bruised credit. Since it is a fast financing option with a higher risk to the lender, interest rates are almost always higher.

“There are costs that just don’t exist anywhere else,” says Phil Soper president and CEO of Royal LePage Real Estate Services, Toronto. There are often costs involved in buying a home that many first time home buyers have never heard of, particularly if they didn’t do their homework or seek good advice during the transaction.

That’s where a realtor can come in handy, says Elton Ash, regional vice-president of Re/Max Western Canada, Vancouver.

“You’re paying a realtor for a service,” says Soper. “That service goes well beyond simply sales service. The realtor should be willing to take the novice purchaser through the entire process, including a summary of all the costs and steps necessary to…

“There are costs that just don’t exist anywhere else,” says Phil Soper president and CEO of Royal LePage Real Estate Services, Toronto. There are often costs involved in buying a home that many first time home buyers have never heard of, particularly if they didn’t do their homework or seek good advice during the transaction.

That’s where a realtor can come in handy, says Elton Ash, regional vice-president of Re/Max Western Canada, Vancouver.

“You’re paying a realtor for a service,” says Soper. “That service goes well beyond simply sales service. The realtor should be willing to take the novice purchaser through the entire process, including a summary of all the costs and steps necessary to…

The gap between variable rate mortgage and fixed rate mortgage products has narrowed in recent years. And while fixed rate mortgages are starting to rise they offer certainty in a monthly payment. On the flip-side, variable rate mortgages remain low, but are the riskier of the two choices – so how do you choose?

Your income, lifestyle and risk tolerance will weigh heavily on your decision and will inevitably determine which product suits your circumstance.

Risk versus reward

The appeal of variable rate mortgages (also called adjustable rate mortgages) is that the interest rate is typically lower than that of fixed rate mortgage products. However, the main drawback is the risk involved. Without warning, interest rates could increase…

The gap between variable rate mortgage and fixed rate mortgage products has narrowed in recent years. And while fixed rate mortgages are starting to rise they offer certainty in a monthly payment. On the flip-side, variable rate mortgages remain low, but are the riskier of the two choices – so how do you choose?

Your income, lifestyle and risk tolerance will weigh heavily on your decision and will inevitably determine which product suits your circumstance.

Risk versus reward

The appeal of variable rate mortgages (also called adjustable rate mortgages) is that the interest rate is typically lower than that of fixed rate mortgage products. However, the main drawback is the risk involved. Without warning, interest rates could increase…

Sometimes concepts in the finance world can be tricky. We get so caught up in trying to understand what all the offerings are that we forget to understand the simple things. When is the last time that someone said what a mortgage really is? Or explained why I can only buy a home for $350,000.00. We all have questions in the back of our minds that we don't articulate because we are just too embarrassed. Here are the top five things you are afraid to ask.

Sometimes concepts in the finance world can be tricky. We get so caught up in trying to understand what all the offerings are that we forget to understand the simple things. When is the last time that someone said what a mortgage really is? Or explained why I can only buy a home for $350,000.00. We all have questions in the back of our minds that we don't articulate because we are just too embarrassed. Here are the top five things you are afraid to ask.

Changes to mortgage rules mean that some home buyers in Metro Vancouver's hot housing market may soon get a break when it comes to their loan application.

Changes to mortgage rules mean that some home buyers in Metro Vancouver's hot housing market may soon get a break when it comes to their loan application.

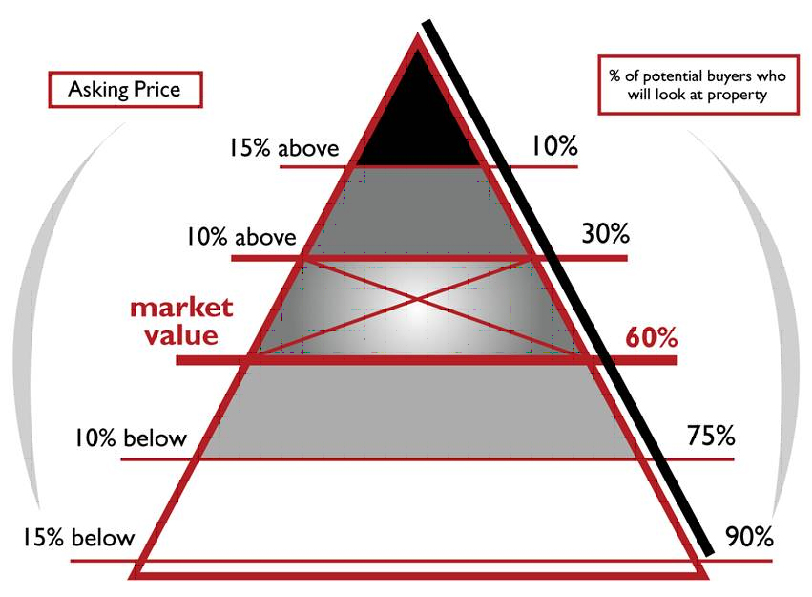

Usually, market value is determined by what a buyer is willing to pay for a home, and what the seller is willing to accept. The recent agreed upon sale price of a home is usually the best determinant of a property's market value. However, there are circumstances where the price paid for a home is not the true market value. For example, there may be a special relationship between the parties which resulted in a much lower value being paid. Also, a buyer may have been willing to pay a premium for a property for some reason, and so it sold for much more than it would otherwise be worth.

Usually, market value is determined by what a buyer is willing to pay for a home, and what the seller is willing to accept. The recent agreed upon sale price of a home is usually the best determinant of a property's market value. However, there are circumstances where the price paid for a home is not the true market value. For example, there may be a special relationship between the parties which resulted in a much lower value being paid. Also, a buyer may have been willing to pay a premium for a property for some reason, and so it sold for much more than it would otherwise be worth.